- Blog -

Transparency In Markets Make Strong Progress (by Research Team at FS Green Professional Services Ltd ABUJA, Aug. 14, 2023/Research-wire/FSGPSL/08:52 CAT)

Transparency improved globally in 2023, with Asia rising as a standout, as real estate markets make progress toward sustainability goals and AI adoption.

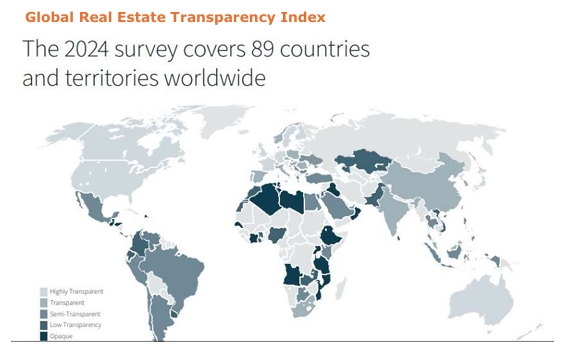

As times of uncertainty endures, Real estate transparency is more critical than ever. And emerging markets are required to be as most transparent as ever before, because they pull further ahead, based on increasing investments in technology integration, AI, data availability and environmental sustainability. This is according to our biennial research on Global Real Estate Transparency Index (GRETI), which benchmarks market transparency to help inform how real estate investment flows in emerging markets compared to developed world.

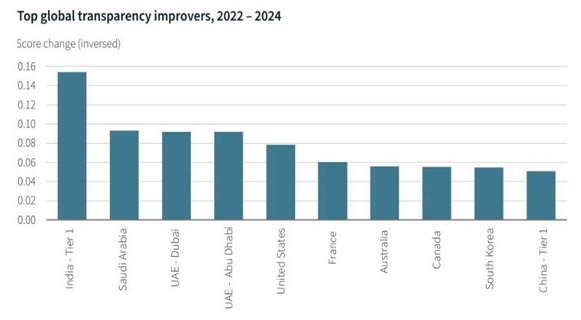

While transparency has increased across most nations and territories since COVID, the recent index finds that Europe remains the most transparent region, and highly transparent commercial real estate markets have seen the strongest progress. Among the global top improvers are the U.S., Canada, France, and Australia, while Singapore has entered the 'Highly Transparent' group for the first time, boosted by a focus on sustainability and digital services. The top set of countries has attracted over $1.2 trillion in direct commercial real estate investment over the last two years, representing over 80% of the global total, positioning them to lead the cyclical recovery in liquidity as capital market activity increases.

In step with Singapore, countries in Asia have recorded the strongest average transparency improvements since 2022. Globally, India is the top improver in transparency, with greater data coverage and quality across property sectors ranging from industrial to data centres.

Japan, Australia, cities in Mainland China, South Korea, the United Arab Emirates, and Saudi Arabia also saw progress in 2023. By contrast, the Sub-Saharan Africa region saw the least progress in transparency, though some signs of improvement emerged in Kenya, Nigeria, and Ghana.

Japan, Australia, cities in Mainland China, South Korea, the United Arab Emirates, and Saudi Arabia also saw progress in 2023. By contrast, the Sub-Saharan Africa region saw the least progress in transparency, though some signs of improvement emerged in Kenya, Nigeria, and Ghana.

"The focus on transparency for investors has never been greater in global real estate markets as external challenges such as geopolitical tensions and election cycles draw increased attention in the near term," said Adeboye Hafeez, Principal Partner at FSGPSL.

"On the horizon, additional drivers like artificial intelligence and higher standards of sustainability obligations and reporting will continue to push investors to seek greater transparency."

"Highly transparent markets in this year's Index represent over half of income-producing real estate worldwide. Countries with transparent pricing and fundamentals, especially across the diverse range of specialty sectors and sub-sectors, will likely lead the real estate liquidity recovery," said Brian Eronmosele, Head of Research Team at FSGPSL.

AI and sustainability drive new transparency opportunities and challenges.

The proliferation of AI has been rapid, hastening expectations for its impact on real estate. It is estimated that over 500 companies are currently providing real estate-specific AI services, and with investment growing significantly, early findings suggest AI will boost transparency across the industry with its ability to review and summarize large volumes of data and analytics, automate building management, and power urban and architectural design. However, experts and policymakers have raised the risks of AI and introduced policies such as the U.S. Executive Order on AI and recently approved EU AI Act to ensure the responsible deployment of the technology to maintain transparency.

In parallel, sustainability marked the largest improvement in the 2023 Index, as nations race to halve carbon emissions by 2030 to meet the Paris Agreement, and the introduction of mandatory decarbonization pathways set new building performance standards, sustainability reporting requirements, and corporate commitments. France, Japan, and the U.S.- with 40 U.S. cities committed to passing a Building Performance Standard requiring building energy use or emission reductions by 2026 – emerged as leaders in sustainability for implementing energy performance requirements for both existing and new buildings, energy use reporting, and biodiversity protection and restoration. These markets with the clearest long-term pathway to more sustainable real estate will offer the most transparent and predictable environments, allowing occupiers to make decisions with confidence, governments to meet decarbonization targets, and investors to future-proof their portfolios.

However, despite significant progress made, sustainability metrics continue to be among the least transparent globally. Beyond the most transparent markets, mandatory building performance standards, public disclosure of buildings' energy use, climate risk reporting, and resilience planning are still limited. The rate of building decarbonization retrofits will need to triple to align with net zero carbon pathways, while demand for green buildings significantly outstrips demand – only 30% of demand for low carbon office space in the major global markets is likely to be met by 2030. Looking ahead, sustainability transparency is expected to grow over the next two years across the world's largest economies including the U.S., EU, U.K., China, Japan, Korea, Canada, and Australia as new requirements are enacted.

With these emerging trends, such as technology integration and sustainability, comes diversification, as investors look to identify assets that will benefit most from these long-term themes. This is resulting in an expansion of the investible universe, and a significant reallocation of capital; the share of global investment into the industrial and living sectors has risen from 29% ten years ago, to account for 50% of global direct investment over the past year, while institutional investors are increasingly active in emerging asset types such as data centres or lab space.

Debt markets, money laundering, and beneficial ownership are among key transparency themes to watch

Approximately US$3.1 trillion of global real estate assets have maturing debt between 2024 and 2025, and US$2.1 trillion of debt will need refinancing.

Roughly 30% has been completed over the first half of 2023; however, monetary authorities have raised concerns about the potential risks from the relative lack of transparency as non-bank lenders expand and complement traditional sources of credit. While commercial real estate lending was historically dominated by regulated banks, the lender landscape has broadened with new credit sources such as debt funds, pensions and insurance companies emerging. This diversification has created a more balanced market, but also one with less visibility into financing conditions in many countries, raising new transparency concerns.

Alongside debt markets, money laundering and beneficial ownership regulations have surfaced as transparency areas to watch. New guidance from the Financial Action Task Force (FATF), requiring countries to ensure they can track the true ownership of companies, paired with widening financial sanctions regimes, have maintained momentum for improving anti-money laundering (AML) and beneficial ownership (BO) regulations. Despite global action, the effectiveness of these regulations remains under scrutiny as implementation and definitions are often inconsistent and easy to circumvent. Countries such as India, Indonesia, the United Arab Emirates and the U.S have introduced changes to AML and BO regulations to help drive transparency, and additional regulations are underway in the U.S., Singapore, Switzerland, Canada, Australia, and the EU.

Global Real Estate Transparency Index (GRETI)

Global Real Estate Transparency Index (GRETI), which is published every two years, is a unique benchmark of market transparency for property investors, developers and corporate occupiers. The index evaluates the legal and regulatory environment, enforcement mechanisms and data availability and provides a global comparison of operating conditions across a wide range of geographies. This year's 3rd edition includes 256 individual indicators to assess market transparency across 89 countries and territories and 151 cities globally.

"The focus on transparency for investors has never been greater in global real estate markets as external challenges such as geopolitical tensions and election cycles draw increased attention in the near term," said Adeboye Hafeez, Principal Partner at FSGPSL.

"On the horizon, additional drivers like artificial intelligence and higher standards of sustainability obligations and reporting will continue to push investors to seek greater transparency."

"Highly transparent markets in this year's Index represent over half of income-producing real estate worldwide. Countries with transparent pricing and fundamentals, especially across the diverse range of specialty sectors and sub-sectors, will likely lead the real estate liquidity recovery," said Brian Eronmosele, Head of Research Team at FSGPSL.

AI and sustainability drive new transparency opportunities and challenges.

The proliferation of AI has been rapid, hastening expectations for its impact on real estate. It is estimated that over 500 companies are currently providing real estate-specific AI services, and with investment growing significantly, early findings suggest AI will boost transparency across the industry with its ability to review and summarize large volumes of data and analytics, automate building management, and power urban and architectural design. However, experts and policymakers have raised the risks of AI and introduced policies such as the U.S. Executive Order on AI and recently approved EU AI Act to ensure the responsible deployment of the technology to maintain transparency.

In parallel, sustainability marked the largest improvement in the 2023 Index, as nations race to halve carbon emissions by 2030 to meet the Paris Agreement, and the introduction of mandatory decarbonization pathways set new building performance standards, sustainability reporting requirements, and corporate commitments. France, Japan, and the U.S.- with 40 U.S. cities committed to passing a Building Performance Standard requiring building energy use or emission reductions by 2026 – emerged as leaders in sustainability for implementing energy performance requirements for both existing and new buildings, energy use reporting, and biodiversity protection and restoration. These markets with the clearest long-term pathway to more sustainable real estate will offer the most transparent and predictable environments, allowing occupiers to make decisions with confidence, governments to meet decarbonization targets, and investors to future-proof their portfolios.

However, despite significant progress made, sustainability metrics continue to be among the least transparent globally. Beyond the most transparent markets, mandatory building performance standards, public disclosure of buildings' energy use, climate risk reporting, and resilience planning are still limited. The rate of building decarbonization retrofits will need to triple to align with net zero carbon pathways, while demand for green buildings significantly outstrips demand – only 30% of demand for low carbon office space in the major global markets is likely to be met by 2030. Looking ahead, sustainability transparency is expected to grow over the next two years across the world's largest economies including the U.S., EU, U.K., China, Japan, Korea, Canada, and Australia as new requirements are enacted.

With these emerging trends, such as technology integration and sustainability, comes diversification, as investors look to identify assets that will benefit most from these long-term themes. This is resulting in an expansion of the investible universe, and a significant reallocation of capital; the share of global investment into the industrial and living sectors has risen from 29% ten years ago, to account for 50% of global direct investment over the past year, while institutional investors are increasingly active in emerging asset types such as data centres or lab space.

Debt markets, money laundering, and beneficial ownership are among key transparency themes to watch

Approximately US$3.1 trillion of global real estate assets have maturing debt between 2024 and 2025, and US$2.1 trillion of debt will need refinancing.

Roughly 30% has been completed over the first half of 2023; however, monetary authorities have raised concerns about the potential risks from the relative lack of transparency as non-bank lenders expand and complement traditional sources of credit. While commercial real estate lending was historically dominated by regulated banks, the lender landscape has broadened with new credit sources such as debt funds, pensions and insurance companies emerging. This diversification has created a more balanced market, but also one with less visibility into financing conditions in many countries, raising new transparency concerns.

Alongside debt markets, money laundering and beneficial ownership regulations have surfaced as transparency areas to watch. New guidance from the Financial Action Task Force (FATF), requiring countries to ensure they can track the true ownership of companies, paired with widening financial sanctions regimes, have maintained momentum for improving anti-money laundering (AML) and beneficial ownership (BO) regulations. Despite global action, the effectiveness of these regulations remains under scrutiny as implementation and definitions are often inconsistent and easy to circumvent. Countries such as India, Indonesia, the United Arab Emirates and the U.S have introduced changes to AML and BO regulations to help drive transparency, and additional regulations are underway in the U.S., Singapore, Switzerland, Canada, Australia, and the EU.

Global Real Estate Transparency Index (GRETI)

Global Real Estate Transparency Index (GRETI), which is published every two years, is a unique benchmark of market transparency for property investors, developers and corporate occupiers. The index evaluates the legal and regulatory environment, enforcement mechanisms and data availability and provides a global comparison of operating conditions across a wide range of geographies. This year's 3rd edition includes 256 individual indicators to assess market transparency across 89 countries and territories and 151 cities globally.